Chess, Computers and the Time Value of Money

Paul Asel

Founding Partner at NGP Capital·

Venture funds are judged on Internal Rate of Return. Partners of the fund receive carried interest based on Return on Investment. Interests are generally but not always aligned. Differences emerge when investors think differently about the time value of money.

Idea in Brief

- Compounding yields high multiples over long holding periods with high rates of return. The benefits of compounding accrue in finance, technology and knowledge.

- The venture industry has benefited from longer holding periods due to the time value of money.

- We may be approaching the second half of the chessboard with artificial intelligence, Moore’s Law and venture holding periods.

The time value of money is not intuitive as business schools across the country struggle to convey the concept. The following two parables underscore the importance of compounding, which underlies the time value of money.

Compounding: A Story of Chess and Computers

The game of chess originated during the Gupta Empire in sixth century India. The emperor was so impressed by this difficult, beautiful game that he invited the inventor to name his reward. The inventor, a humble farmer, said, “All I desire is some rice to feed my family.” Referring to the chess board, the farmer-inventor proposed to start with one grain of rice on the first square and double the amount in each succeeding square. Impressed with the apparent modesty of the request, the emperor replied, “make it so.” One grain turned to two then four then eight then sixteen. Not even a mendicant could live on such rations. But the grains of rice expanded unrelentingly with each square and by the midpoint of the board, the farmer received 4 billion grains of rice, the equivalent of about one large field of rice.

It was only as they moved to the second half of the chessboard that at least one man got into trouble. The seemingly humble request could not be fulfilled. At the end of the chessboard on the 64th square, the farmer would receive 1.8 x 10^19 grains, more rice than has ever been produced.

Intel cofounder Gordon Moore made a similarly humble wager when he proposed in 1965 that semiconductors would double computing power every two years. Initially proposed as a guideline for the following decade equivalent to the 16 grains of rice on the fifth chessboard square, Moore’s ‘Law’ has proven more durable than expected. Computing power once housed in bulky mainframes that would fill a football field now fits comfortably on our wrists as smartwatches. These exponential increases in compute power have driven software and hardware innovation for the past sixty years. With artificial intelligence unleashed as we move toward the midpoint of the chessboard, it may only be in the second half that someone gets hurt.

The Time Value of Money

Investors pay high premiums for expected growth. At $1.5 trillion, Tesla now trades at 15x revenues with a valuation 25 times higher than all other U.S. auto producers combined. With current profit margins, Tesla would need to pay 100% dividends on income for the next two centuries for shareholders to recoup their capital. But investors are not valuing Tesla solely on current performance. They are hoping that Moore’s Law applies to Tesla profitability if not revenues.

The difference between good and great companies (and investment outcomes) may be just a few percentage points when compounded over long time periods. When forecasted revenue slips 5% below budget, the CEO typically explains this as a slight variance, perhaps with a customer deferring an intended purchase by a month or two. But the 5% slip is typically a bigger issue than management suggests. The relevant variation from forecast for a business with subscription revenue is the difference in incremental revenue growth for the year, not total revenue. A 5% slip for a company expected to grow 10% for the year is a 50% miss on incremental revenue growth. The next budget cycle starts with a lower revenue total so this slip in one year will compound in the years ahead.

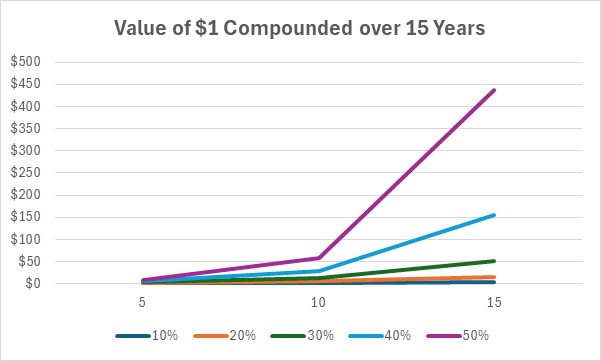

Simple math illustrates why investors pay high premiums for sustained growth. A $1 investment increases 2.6x in ten years with 10% annual growth but 9.3x with 25% growth and 58x with 50% growth. Compounded over fifteen years, which is increasingly the standard life of a seed stage fund, our $1 investment increases to $4.2 with 10% annual growth, $28 at 25% and $438 at 50%. Doubling the growth rate from 25% to 50% increases returns by 15x over fifteen years. The difference is 100x for an increase from 10% to 50% annual growth.

Figure 1: Time Value of Money Compounded over 15 Years with 10-50% Growth Rates

Why Time Value of Money Matters

The time value of money matters more as venture capital holding periods have increased over the past three decades. Venture-backed startups now take twice as long to go public: time from inception to IPO now averages 12-14 years instead of 6-8 years in the 1990s. Startups are scaling faster but staying private longer with larger late-stage funding rounds and secondary markets that permit partial exits for investors who need early liquidity. Staying private longer enables companies to focus on long-term prospects with less public scrutiny and avoid earnings disclosures that give customers and suppliers visibility into profitability that may shift bargaining power and exert pressure on operating margins.

Longer holding periods also benefit venture firms, which can hold winners longer to capture more value. As we observed with compounding in the second half of the chessboard, doubling holding periods can have significant impact on fund returns. Venture firms have doubled or tripled fund Return on Investment (ROI) simply by holding onto future IPOs longer.

Interests of venture firms and their limited partners generally align on longer holding periods but not always. Since they can readily reinvest liquid capital, limited partners focus on time value of money as measured by Internal Rates of Return (IRR). Venture partners earn carried interest based on absolute return independent of time value of money as measured by Return on Investment (ROI) or Multiple on Invested Capital (MOIC). Venture firms and their limited partners both benefit from compounding but limited partners have an opportunity cost of capital and would prefer to sell once incremental annual returns fall below their IRR hurdle rate, while venture firms will be tempted to hold on longer in the absence of incremental carrying costs.

Institutional investors in private equity firms bridge potential misalignment by applying an IRR hurdle rate before PE firms earn carried interest. Venture firms in Europe and Asia also have IRR hurdle rates. But carried interest calculations for U.S. venture firms are fixed so longer holding periods benefit general partners but not necessarily limited partners. An investment that appreciates 10% in the last year before exit, for example, would be below the limited partner hurdle rate for an early-stage venture investor but could earn another 1x ROI for an investment already valued at 10x MOIC. So venture investors and their limited partners also have potential challenges as exit horizons extend and approach the second half of the chess board.

The next decade will be suspenseful as we reckon with the three potential phase shifts in the second half of the chessboard: (1) societal shifts as technology advances toward general artificial intelligence; (2) technical shifts toward quantum computing as traditional semiconductor technology approach physical limits to Moore’s Law; and (3) rising gaps between general and limited partners related to the time value of money as holding periods extend further.

Related Concepts

Time value of money increases proportionally with prevailing interest rates and inflation rates. The time value of money is static if interest and inflation rates are 0% but can escalate quickly as rates increase due to compound interest.

Investors report to limited partners gross and net IRR, which reflect the time value of money. Other reported metrics are based on investment multiples that do not explicitly account for time value of money such as Total Value to Paid-In Capital (TVPI) or Multiple on Invested Capital (MOIC) and Distributions to Paid-In Capital (DPI). Limited Partners assess all reported measures relative to a hurdle rate that reflects the time value of money and perceived risk inherent in the investment strategy. The hurdle rate for early-stage investors typically exceeds 20% due to higher investment risk, while late stage and private equity investors with lower loss rates typically have hurdle rates of 10% or higher.

Given the time value of money, expected holding periods are a key consideration for investors when evaluating the attractiveness of an investment. Duration in fixed income investing is predetermined based on the loan repayment structure. Holding periods are undefined and highly variable for equity investments, so exit strategy and timing should be discussed with companies prior to investment. Exit strategies may shift based on company performance as the time value of money motivates investors to hold their winners and quickly exit underperforming investments.