Impact Investing: Socially Responsible Investing Reimagined

Paul Asel

Founding Partner at NGP Capital·

Impact Investing, long a province of development finance institutions, has moved mainstream. My framework shows how venture philanthropy is more scalable and sustainable, though more ambiguous, than grant funding.

Idea in Brief

- Impact investing recognizes that firms must do well to do good.

- Impact investing explores a range of opportunities between pure financial and social objectives. Two-pocket investors separate funding for financial and social motives. One pocket investors pursue both goals concurrently.

- Impact investing recycles financial returns to fund other worthy causes while grant funding is one and done.

- Impact investing assesses both social and private returns. A concessionary financial return is justified only if social returns more than offset the opportunity cost of financial returns.

- Impact investing success involves additionality and demonstration effects. It should not compete with financial investors, but success should attract financial firms into the market.

Impact investing, an investment strategy that seeks to generate financial returns while creating a positive social or environmental impact, has grown 17% annually the past five years to $715 billion assets under management involving 1720 firms according to a 2020 survey by the Global Impact Investing Network (GIIN). Major financial firms such as Bain Capital, Calvert, Goldman Sachs, JP Morgan, Merrill Lynch, Morgan Stanley, Temasek, Texas Pacific Group now offer impact fund alternatives.

Our analysis shows that entrepreneurs and investors have focused on environmental issues as companies that identify with Sustainable Development Goals (SDGs) from the United Nations has more than doubled over the last two years. A requirement that large institutional investors report on ESG and SDG investment activities has spurred the rise in impact investing. Impact investing now accounts for 7% of all private investment assets under management and more than a quarter of assets under management operate according to ESG principles according to McKinsey.

Yet the growth of impact investing has aroused much skepticism. In “Is ‘impact investing’ just bad economics?,” Philip Demuth at Forbes argues that impact investing muddles financial and charitable motives missing the mark on both measures. Instead, he advised that investing be left to financial managers while charities focus on donations. Others worry about ‘impact washing,’ spurious investor claims of social impact without supporting evidence, a temptation that increases as governments impose ESG (environmental, social and governance) mandates.

Economic Merits of Impacting Investing

Dismissing impact investing altogether as Demuth does is bad economics. Impact investing, like effective financial investing and charitable donations, require nuanced judgment and intellectual rigor. When thoughtfully administered, impact investing applies sound economic principles that accomplishes investment and charitable objectives more effectively jointly than when pursued separately.

Microeconomics is a balancing act. Production optimizes where marginal cost and marginal productivity intersect. Consumption optimizes where price equals marginal utility. Manufacturers maximize production by balancing capital and labor. Consumers maximize utility by balancing work and leisure and allocating discretionary spending across a basket of goods. Similarly, impact investing seeks to optimize financial and social mandates by balancing these objectives across an asset portfolio.

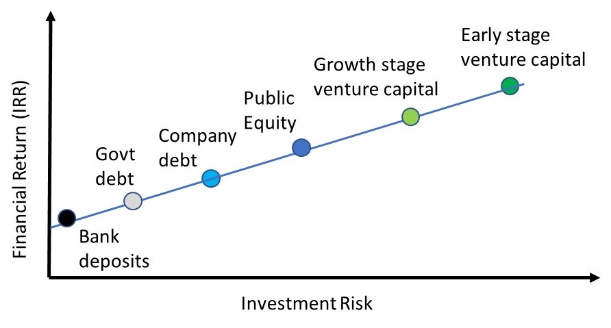

Financial economics describes an ‘efficient frontier’ as the optimal expected return for a given level of risk. As shown in Exhibit 1, investors require a higher return on illiquid, risky venture capital investments than liquid, low risk government securities or bank deposits.

Exhibit 1: Efficient Frontier and Market Rates of Return

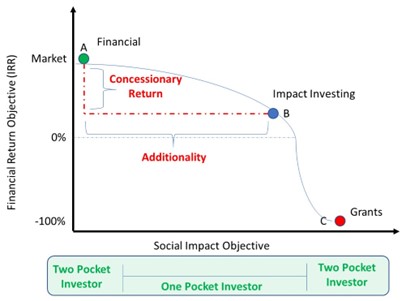

The efficient frontier framework also applies to impact investing by associating required financial return for a given level of social impact. A pure financial investment requires a risk-adjusted market rate of return independent of social impact. A grant requires high social impact to compensate for foregone financial return.

Impact funds offer a middle path between these two extremes. They seek to do good while doing well offering financial returns while delivering positive societal impact. Financial and social objectives are not mutually exclusive. Conscientious financial investment contributes positively to society. Venture capital has brought life changing innovations, economic growth, prosperity and employment wherever it has flourished. Financial returns and social impact are often mutually reinforcing. No activity can do good if it does not do well: underperformance is unacceptable to donors and investors alike.

Impact investing involves real tradeoffs. Surveys indicate that 67% of impact investing assets under management are deployed for risk adjusted market rates of return. The other 33% accepts concessionary returns while seeking to return capital. As Exhibit 2 shows, concessionary returns may be economically efficient if an investment provides sufficient additionality through social benefits that could not otherwise be achieved through financial objectives exclusively.

Exhibit 2: Efficient Frontier for Impact Investing

Impact Investing Advantages Relative to Grant Funding

Grant funding addresses social needs in the non-profit sector where market friction obstructs for-profit initiatives. Sources of market friction are manifold. Public goods, externalities, knowledge spillovers, low-income markets with limited ability to pay, high transaction costs, frontier markets with political uncertainty, institutional constraints and regulatory uncertainty are just a few of the market frictions that many worthy non-profit organizations address.

Yet not all activities fit neatly into a bifurcated world of financial investment and social goods. Two by two matrices have intellectual appeal, yet bipolar worlds are bleak and disordered as evidenced by our current partisan political malaise. Impact investing thrives in the more nuanced world in which we live.

The economic principle of money velocity illustrates the advantages of impact investing. Money velocity measures the number of times currency is used to purchase goods and services during a given time period. A supermarket with weekly inventory turns will have 26x higher money velocity than a car dealership with semi-annual inventory turns. Increased money velocity produces higher economic growth all else being equal.

Impact investing offers a return of capital while grant funding involves a single use of donor capital. Donor capital is gone once deployed, while impact investing capital, even when deployed at concessionary rates, uses capital multiple times. Capital can be recycled five times with an 80% return of capital including administrative expenses and ten times with a 90% return. A 100% return of capital may be redeployed indefinitely, and profitable returns offer a growing source of committed capital.

Fundraising for impact investing can be a tough sell despite its evident advantages over grant funding. Jacqueline Novogratz, founder of Acumen Fund, observed the challenges of pitching impact investing: “It never fails to amaze me how people seem comfortable making grants for purely charitable purposes so they experience a 100% loss of their money and are equally comfortable investing in hopes of seeing financial returns of 10-20%, even if they risk losing a portion of principal. Yet these same individuals will often not consider investments with outsized social impact that result in negative returns of 10-20%. Between pure charity and pure financial return, there is an unexplored space with tremendous opportunities for innovation, social impact and lasting change.”

This comment highlights the distinction between a two pocket versus one pocket investor. By separating financial investments and charitable contributions, two pocket investors commit capital at the far edges of the investment range in Exhibit 2. Impact investing apportions capital along the continuum offering a range of financial returns with social impact.

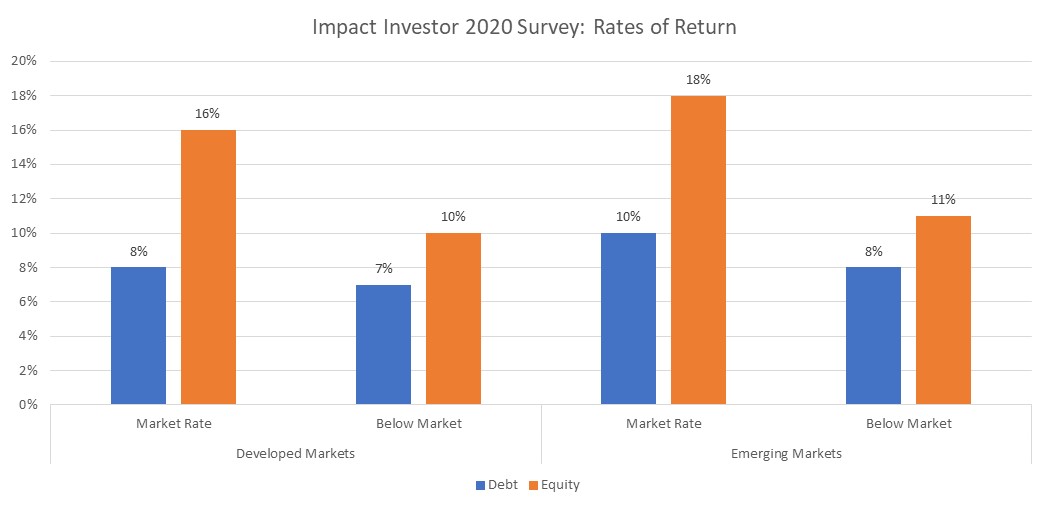

The entry of top tier investors into impact investing suggests attractive financial returns and market demand among one pocket investors. As Exhibit 3 shows, impact investors report 10-18% median equity returns and 7-10% debt returns across developed and emerging markets according to a 2020 survey by the Global Impact Investor Network. Median concessionary discounts for below market versus market rate investors are 10-20% for lenders and 40-50% for equity investors.

Exhibit 3: Impact Investor Reported Rates of Return

Impact Investing: Social Returns and Demonstration Effect

Impact investing works when social returns on an initiative exceed private returns. Inventors do not capture the full value of their inventions as meaningful new technologies, ideas and processes have applications far beyond their initial use case. Similarly, impact investors may accept concessionary private returns when social benefits more than offset foregone opportunity realizable from a purely financial investment.

Impact investors have found an untapped market opportunity for socially responsible investing. Investors who can demonstrate substantial additional social benefits while minimizing the opportunity cost of concessionary private returns.

But one pocket investors serve two masters when balancing dual objectives. Impact investors deal with ambiguity when balancing social benefits with expected financial returns. The growth of impact investing complicates balancing these dual objectives. The fungibility and growing popularity of impact investing risks abuse as a marketing ploy rather than a separate discipline. Impact investing may simply drive valuations up for financial investors if they compete for the same investments. Impact investing fulfills its mission only if there is additionality: it adds value that financial investors could not provide or invests in overlooked sectors where market friction exists.

Yet market friction abounds as investors systemically overlook frontier markets due to limited liquidity, political uncertainty, institutional constraints and exit options. Frontier markets with 50% of the world population receive just 5% of global private investments representing just 0.4% of global market capitalization. Investments in public health, education, energy, agriculture, the environment and community enablement involve positive externalities with social benefits far exceeding private returns. Over 40% of the world adult population are unbanked ignoring wealth at the bottom of the pyramid due to small transaction sizes and imperfect information. Without government support through patent protections and funding for basic research, the private sector systematically underinvests in research as scientific breakthroughs involve knowledge spillovers that no single entity cannot fully capture.

Impact investing at its best attracts mainstream capital into previously overlooked markets. The International Finance Corporation was an early investor in leading emerging market mobile operators such as Airtel in India, MTN in Africa and Orascom in the Middle East accelerating mobile adoption across emerging markets and attracting private investment. Microlenders Grameen Bank in Bangladesh, SKS Microfinance in India, BancoSol in Bolivia demonstrated profitable small lending to unbanked borrowers attracting bank competition and over $152 billion of capital to an overlooked sector. MPesa in Africa, Alipay in China and PayTM in India have created robust mobile payment systems that have bolstered the digital economy in their respective markets and spurred emulation across other emerging markets.

Impact investing is dedicated to the view that we sleep better when our capital offers financial returns while pursuing socially responsible objectives. While grant funding has its place, impact investing explores the broad range of opportunities that pursue worthy missions within the market context. We applaud the World Business Council for Sustainable Development and its coalition of 120 international companies who share a commitment to the environment, sustainable development and economic growth.

Related Concepts

Impact Investing relies on return on investment (ROI) but involves both financial and social returns. Successful impact investors should be on the efficient frontier on a financial/social return matrix, though key metrics for social returns vary and are often subjective. Grant funding may be treated as a sunk cost without expected returns, while impact investing benefits from a money multiplier through reinvestment of returns for other worthy causes.

Impact investing involves moral hazard as the dual objectives of financial returns and social benefits permit a wide range of investment justifications. Impact investors should have clear guidelines and apply investment filters to test for both financial and social returns and possibly for additionality (not competing with financial investors) depending on the funds mandate. Thesis driven investing also helps focus on target areas that meet both criteria.