Three Cardinal Sins of Investing: Reducing Errors of Omission When Assessing Disruptive Startups

Paul Asel

Founding Partner at NGP Capital·

Lucrative outcomes require investing in the right market with the right team. Savvy seed investors focus on insights to identify superior teams pursuing disruptive innovation where prior experience is not a reliable guide.

Idea in Brief

- Founder Market Fit frameworks are attuned to incremental innovation where prior experience is a reliable guide for future success but often mislead when assessing disruptive innovation.

- Many desirable founder traits are consistent across startups, but we discuss several measures that differ depending on the nature of the startup.

- Founder insight is a better guide for disruptive innovation where experience is less meaningful. We discuss methods to more reliably assess founder insight.

What do Amazon, Alibaba, AirBnB, Bentley Systems, Cisco, DataDog, PagerDuty, Peloton, Pinterest, Robinhood, SquareSpace, Uber, Udemy and UIPath have in common?

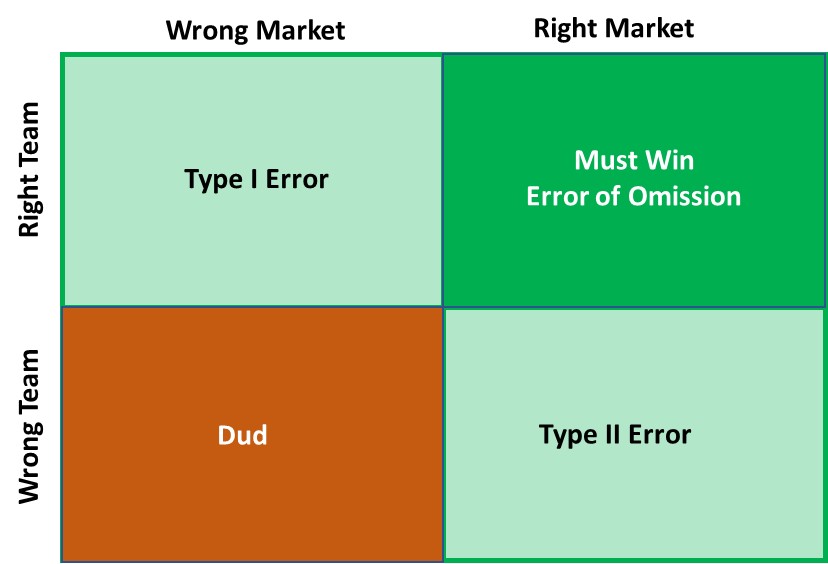

In Secrets of Sand Hill Road, Scott Kupor described the three cardinal sins of venture capital: (1) investing in the right team but wrong market; (2) investing in the right market but wrong team; and (3) not investing in the right market with the right team. Investors rarely err by backing the right team as an A team can sometimes make a B plan work or pivot to a better place. Investing in the wrong team is painful as it may preclude other investments in lucrative markets. Opportunities to invest in markets that produce large, outsized returns are rare so passing on the right team in the right market is especially painful.

So painful that Bessemer Venture Partners, one of the nation’s oldest venture firms, publishes “The Anti-Portfolio” to honor successful companies it missed and remind investors to pause before passing on odd ideas and teams. The Anti-Portfolio includes AirBnB, Apple, eBay, Facebook, FedEx, Google, Intel, Paypal and Tesla. As Bessemer notes, “if we had invested in any of these companies, we might not still be working.”

Bessemer is not alone. Investors routinely pass on high potential teams pursuing disruptive ideas. Amazon, AirBnB, Bentley Systems, Cisco, DataDog, PagerDuty, Peloton, Pinterest, Robinhood, SquareSpace, Uber, Udemy and UIPath are publicly traded unicorns that together are valued at over $2.5 trillion. Yet they all had difficulty raising their first round of funding. Jeff Bezos spent over a year raising Amazon’s first financing round. AirBnB, Pinterest, Robinhood and Udemy founders claimed that over 100 venture firms initially passed on their startups. John Foley said raising the first three rounds for Peloton was ‘bone crushing.’ Y Combinator rejected Alex Solomon, founder of PagerDuty, four times before admitting him on the fifth try after he had already achieved product market fit. Bentley Systems, SquareSpace and UIPath founders bootstrapped their businesses for over fifty years cumulatively before raising financing.

Nearly half of the disruptive technology firms with unicorn IPOs in the past decade claimed to have difficulty raising funding. Hundreds of top U.S. venture firms committed the third cardinal sin of investing in these businesses: they made a fund making error of omission and passed on a startup with the right team going after the right market.

Table 1: The Three Cardinal Sins of Investing

Successful venture investors use pattern recognition to make investment decisions. We meet thousands of entrepreneurs and review hundreds of funding pitches annually. Investors reliably apply pattern recognition for startups promoting incremental improvements led by founders with demonstrated success in industries they are pursuing. Pattern recognition for disruptive startups is harder as founders typically come from outside the industry and lack telltale markers of success. Yet disruptive innovation produces the largest outcomes, so pattern matching is least attuned for ventures that matter most.

Founder Opportunity Fit: Pattern Recognition Challenges

Two challenges explain low hit rates assessing founders of disruptive startups: (1) these entrepreneurs appear to lack traits that investors seek; and (2) investors misread founder potential without these telltale markers. Research suggests that both factors apply.

Successful entrepreneurs are diverse and rarely conform to central casting. Few investors would wager on the following profiles:

- Adopted child. College dropout. Fired from first company. Unkempt and rarely showered. Cheated his cofounder out of 80% of his annual bonus.

- Failed college entrance exam twice due to weakness in math. Worked at Kentucky Fried Chicken after being rejected for 31 jobs after college. Went into teaching after his first company failed.

Those who declined passed on Steve Jobs at Apple and Jack Ma at Alibaba. Masayoshi San of Softbank invested in Alibaba claiming that Jack Ma had the “scent of an entrepreneur.” Sounds like Steve could have used some of Jack’s cologne during his long intervals between showers!

If there is a scent of an entrepreneur, then investors need to adjust their olfactory senses. Investors, like all people, are susceptible to the liking bias and invest in people with shared traits and backgrounds. Since funds and startups require different skills, investors may be drawn to the wrong sorts of folks. Management assessment systems are highly subjective, risk reinforcing existing biases, and are readily reverse engineered for desired outcome.

Biases compound in hot markets when overconfidence and the Fear of Missing Out (FOMO) prevail. Charlie Munger warns of a “Lalapalooza Effect” when multiple biases converge. Receding tides show who is swimming naked as observed with now bankrupt FTX where funds caught in the cryptocurrency craze invested $1.8 billion without any board oversight. Sam Bankman Fried had all the right credentials but lacked operating experience and would have benefited from some oversight.

Founder Fit Investment Criteria for Disruptive v. Incremental Innovation

Great challenges present great opportunities. Leadership is the most important factor for startup success as Jim Collins noted in Good to Great: “First who … then what.” Conversely, Peter Thiel from Founders Fund observed: “A startup messed up at its foundation cannot be fixed.”

Entrepreneurship requires a diverse skillset. The varying nature of startups enables founders to find opportunities that play to their strengths. Operators focus on process innovation while strategists identify gaps in the market and technologists focus on deep tech innovation.

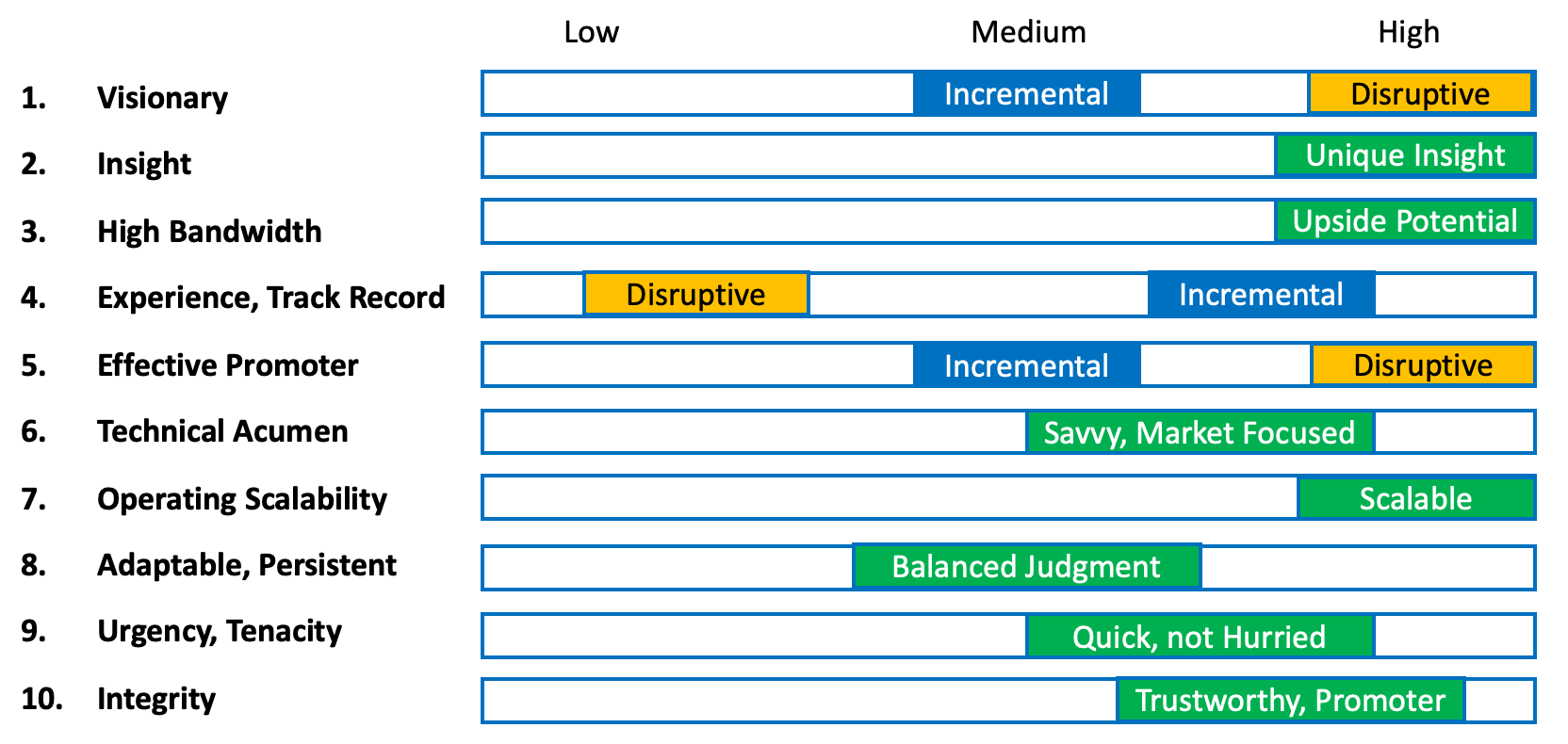

Investors have varying preferences, but they tend to converge on a set of common characteristics. Investors seek entrepreneurs with unique insights and the capacity to fully exploit the opportunity. They value promoters who can sell the idea without deluding themselves on challenges that await them. They seek founders with the persistence and tenacity to overcome obstacles tempered by the balanced judgment to pivot when needed. Founders should have a sense of urgency and be quick without hurrying. Above all trust and integrity are essential. As Table 2 illustrates, many founder attributes are both subjective and nuanced: a high score is preferred for some while a medium or low score is better on other measures.

Table 2: Selected Startup Leadership Traits

Founder fit varies based on the nature of the opportunity. A deep tech investment requires technical capacity, while a business model innovation requires strategic insight and process innovation requires operating scalability.

Requirements for incremental and disruptive innovation vary across at least three dimensions. Disruption often emerges from an outsider’s perspective while incremental innovation requires more industry experience to appreciate where current solutions can be improved. Disruptive innovation often requires a more visionary approach and stronger promotional capacity than incremental innovation in established markets. Table 2 highlights these differences in the first, fourth and fifth attributes.

The traditional guideposts that investors use to assess founders and markets often disappear in the fog of disruptive innovation. Founders promoting disruptive innovation are often industry outsiders pursuing unproven opportunities where market potential is murky.

Insight Driven Investing: Founder Fit for Disruptive Innovation

Founder insight is a better guide for disruptive innovation where experience is less meaningful. Founder insight derives from one of four sources: incremental innovation from (1) prior industry experience or (2) knowledge spillovers from founder networks and disruptive innovation from (3) technical or lead user insight or (4) first principle thinking.

The Contrarian Question that Peter Thiel espouses in Zero to One applies well when assessing disruptive innovation: “What important truth do very few people agree with you on?”

Disruptive innovators are iconoclasts who can respond affirmatively and with conviction to answer this question. Contrarian thinking is useful to entrepreneurs only if it produces meaningful, timely and valuable insights. Entrepreneurs should be able to explain how their insight meets these three criteria.

The Contrarian Question also invites the founder to share his or her journey developing a different perspective. Investors should seek to ascertain the level of conviction and suppleness of thinking in arriving at this point of view. Ultimately, exploring the thought process elicits a better understanding of the balanced judgment needed to decide when to persistent or pivot when obstacles emerge while converting this insight into opportunity.

The Contrarian Question and assessing disruptive opportunities is a litmus test for both the investor and entrepreneur. The founders of Amazon, Alibaba, AirBnB, Bentley Systems, Cisco, DataDog, PagerDuty, Peloton, Pinterest, Robinhood, SquareSpace, Uber, Udemy and UIPath already had conviction to pursue their startup. The question is more often which investors are sufficiently supple to appreciate a lucrative opportunity even when presented in a primordial form.

Most investors missed and committed the third Cardinal Sin of Investing. Hopefully this framework helps investors better answer the Contrarian Question and appreciate the unconventional thinking of founders promoting high potential opportunities when few others do.

Three Cardinal Sins of Investing: Related Concepts

The Three Cardinal Sins of Investing involve misevaluations of founders and markets and highlight the importance of correctly assessing Founder Opportunity Fit and Product Market Fit. Investors must consider the Opportunity Cost of investing in the wrong team if it precludes future investments in a high potential market. Adverse Selection applies when investors use suboptimal methods for founder assessments.

Many factors complicate startup founder evaluations. Radical or 0 to 1 Innovation often emerges from outsiders, so industry experience may be a negative indicator for disruptive startups. Information Asymmetry is most pronounced in early-stage investments, so investors routinely pass on spaces they do not understand well. Cognitive biases, especially Like Bias or Associative Bias, may be more prevalent in early stage investing where there are few objective guideposts.

Power Law Distributions where 80-90% of venture returns come from 10-20% of invested capital highlight the importance of correctly assessing Founder Fit. Investing in a great founding team increases Margin of Safety as they can course correct if their initial plan proves unsuccessful. Improving founder assessments offer a Sustainable Competitive Advantage for investors as decision systems are neither visible nor readily replicable by others.